More updates: Paycheck Protection Program loan deadline extended

Update 7/6/2020: The deadline to request a loan from the Paycheck Protection Program has been extended to August 8, 2020. As of July 6, about $130 billion is still available for loans, which can be forgiven if the proceeds are used for payroll, rent, and other approved expenses. Keep reading to learn how to apply for a PPP loan for your business.

Update: The recent passage of the Paycheck Protection Flexibility Act makes changes to the requirements for loans to be forgiven. It extends the covered period to 24 weeks, increases the length of time allowed to rehire employees who have been laid off, and decreases the percentage that must be spent on payroll to 60%.

President Trump just signed the $2.2T CARES (Coronavirus Aid, Relief, and Economic Security) Act into law to provide economic relief for those affected by the current pandemic. Here’s what small business owners need to know.

What is in the CARES Act?

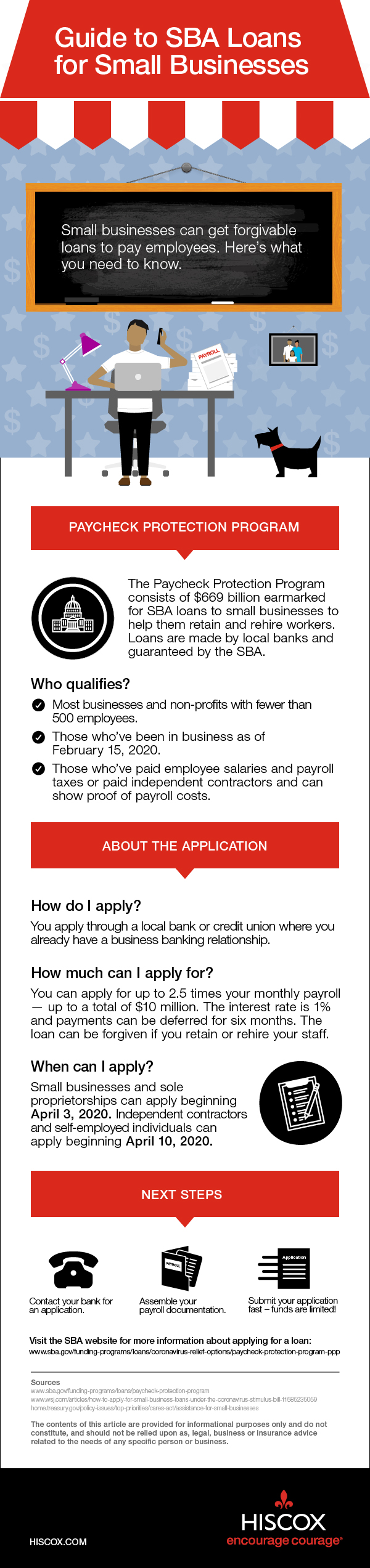

The CARES Act consists of three major components:

- Loans for struggling businesses (including funds specifically earmarked for businesses with 500 or fewer employees), called the Paycheck Protection Program.

- Expanded unemployment benefits, including an additional 13 weeks of benefits, and up to $600 more per week in benefits for up to four months. Self-employed and gig workers will also be covered.

- Payment of up to $1,200 to each individual or $2,400 to each couple, plus $500 for each child under 16. These payments would be phased out for those with incomes over $75,000 ($150,000 for couples).

How will the new stimulus package help small business owners?

For business owners, the part of this plan that may provide the most immediate relief is the Paycheck Protection Program, which provides low-interest loans for small businesses being hit hardest by the outcomes of the pandemic. Here’s what business owners can expect:

- Loans will be handled through the Small Business Administration’s existing 7(a) program. Loans are made by private lenders (banks, credit unions, and other lenders) and are guaranteed by the SBA.

- The self-employed, including gig workers like Uber and Lyft drivers, are eligible.

- The amount that can be borrowed is dependent on your payroll expenses, so you must have paid employee salaries and payroll taxes, or have paid independent contractors. You’ll need to show proof of these payments.

- The purpose of these loans is to provide a cushion so that employers can continue to pay their employees, or can rehire those they have already let go. Part or all of the loan may be forgiven for employers who retain or rehire workers.

How to apply for a loan

To apply for a loan, go to your current bank and see if they can offer you a loan under this program. There are about 1,800 lenders who are currently authorized to make these loans, and Treasury Secretary Steven Mnuchin has said there are plans to allow any FDIC-insured lender (which includes virtually every bank) to offer these loans.

For more information on SBA loans and the CARES Act, visit the SBA website. Click here for more information from the Internal Revenue Service on the Paycheck Protection Program.

Also, follow our guide to find out how to apply.

Unemployment expansion

The CARES Act increases unemployment benefits for those who have been laid off. The Act extends the period of time that out of work people can collect unemployment benefits for an additional 13 weeks. It also increases the amount of compensation they can get by up to $600 per week. More details are available in this announcement from the Department of Labor.

Unemployment benefits are managed by each state, but they all follow the federal guidelines. If you have had to lay off employees, encourage them to file for unemployment by visiting their state’s unemployment website. The Department of Labor website has information about unemployment insurance and a link to each state’s website.

The contents of this article are provided for informational purposes only and do not constituent, and should not be relied upon as, legal, business or insurance advice related to the needs of any specific person or business.

Related Articles

What is Primary Insurance?

Learn the difference between primary and excess insurance, how primary coverage works, and why clients require primary policies.

Learn more

Learn the difference between primary and excess insurance, how primary coverage works, and why clients require primary policies.

Why do you need fitness trainer insurance?

Learn about the insurance every personal trainer needs to have. Protect your personal training business with personal trainer insurance.

Read More

Focus on liability insurance: does my commercial lease need it?

If you're running your small business using a commercial space you may be wondering if your commercial lease requires you to carry liability insurance. Here's what you need to know.

Read MoreWe provide tailored insurance for the specific risks you face, so you can take the right risks to grow your business.

Subscribe to the Hiscox Entrepreneurial Digest on LinkedIn

Get valuable business resources, timely tips and inspiring success stories in your LinkedIn feed every month.