The 2018 Hiscox Embezzlement Study: An insider's view of employee theft

Small business owners often think of their employees as family, and they trust them as such. That’s why it’s such a betrayal when an employee steals from the company – yet it happens far more frequently than you might think. And it goes much further than a staff member with their hand in the till.

The 2018 Hiscox Embezzlement Study™: An Insider’s View of Employee Theft shows how companies can be victimized and how much it costs them. We surveyed chief financial officers, controllers, and accountants who have witnessed the consequences of embezzlement firsthand at the companies they worked for.

Download the report to learn about the impact of employee theft and how you can prevent, detect, and mitigate it at your own company.

The high cost of employee theft

When most people think of embezzlement, they think of Wall Street fraudsters or complicated schemes to beat casinos at their own game. The phrase ‘employee theft’ conjures images of retail employees stealing cash from the register or clothes off the rack. The reality is quite different from both of these scenarios.

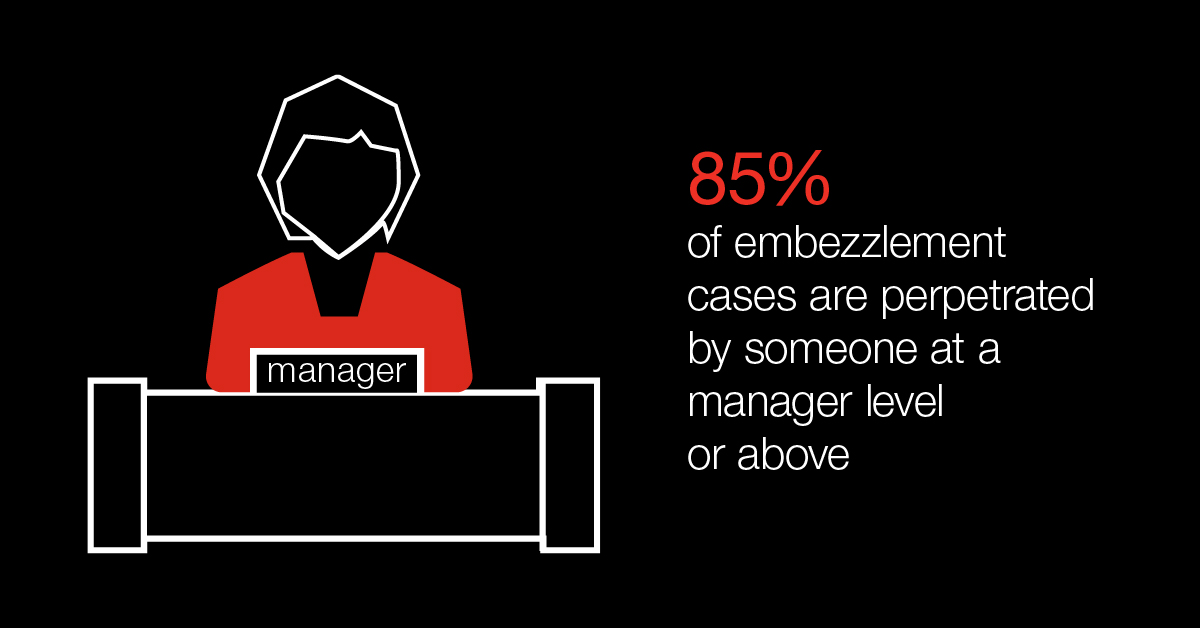

The study found that the average case of employee theft was perpetrated by three people in the same organization, at least one of whom was at the manager level or above. Most cases went on for more than a year before they were discovered. The average loss was $357,650, and just 39% of that was ever recovered by the company, through settlements, restitution or insurance.

The economic repercussions of employee theft extended far beyond the stolen funds. Many companies had to lay off employees because of the theft, and many lost customers or vendors or had trouble attracting new ones. It was common for companies to increase their spending on auditing and security measures as the result of a theft.

How to spot an embezzler

Embezzlers get away with their crimes by flying under the radar. But there are often warning signs, and recognizing them can help you nip fraud in the bud. Look out for:

- employees who seem overly curious about company processes – especially those that are outside their scope of responsibility. If your purchasing agent is asking detailed questions about the payroll function, you may want to take a closer look

- an extravagant lifestyle that’s out of proportion to their salary. The accounting clerk who drives a luxury car and takes expensive vacations should raise a red flag

- risk-taking, in and out of the office. Those who steal often take unnecessary risks in other areas of their lives as well.

- those who come in early, stay late and rarely take vacations. This behavior is often viewed as dedication or ambition, but may actually be due to a desire not to get caught.

As with any crime, a thief must have the means, motive, and opportunity to commit their crime. An employee with detailed knowledge of a company’s accounting practices, a desire to steal that may be fueled by desperation or entitlement, and access to the company’s cash or credit can concoct a scheme that goes undetected for years.

Three steps to protect your company

You can reduce your chances of becoming a victim of employee theft by following these three steps.

- Prevent theft before it happens. Create a system in which statements, checks, and invoices are reviewed by more than one person. Have bank statements delivered to the owner’s home rather than the business address. Perform background checks, as allowed by law, on everyone, but especially those who will handle money.

- Detect theft early. Watch for unusual behavior by a single person or a group. Don’t assume that longtime employees are immune from the greed that drives employee theft.

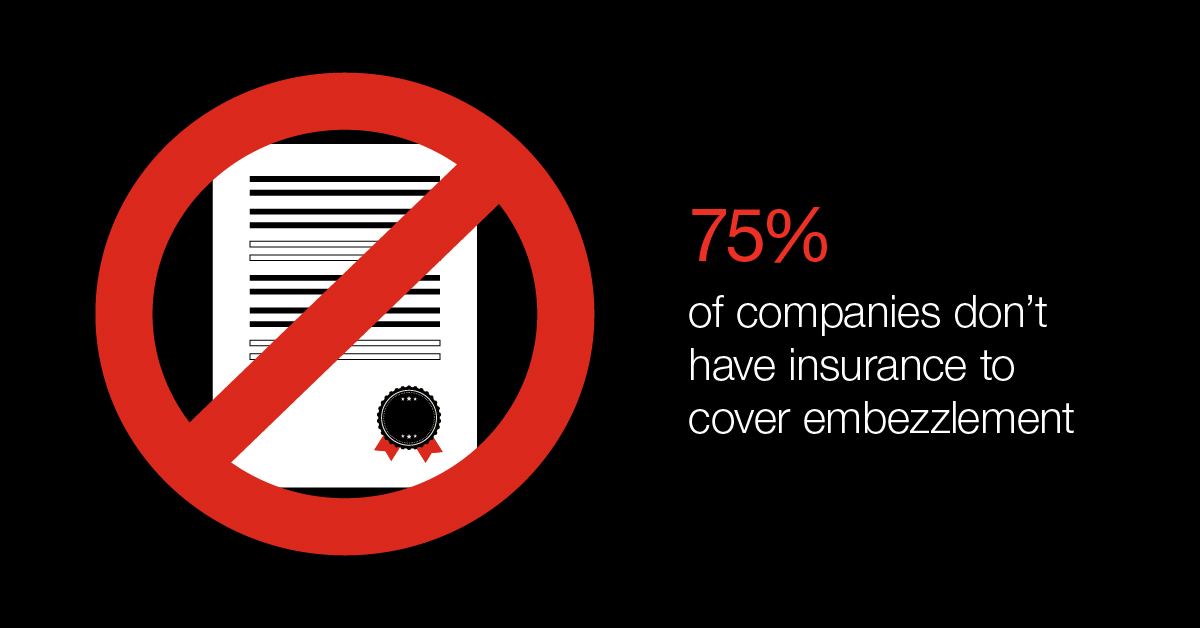

- Mitigate that impact on your bottom line. If you catch someone stealing from you, press charges. This sends a message to other employees that theft won’t be tolerated, and prevents the perpetrator from plying their trade at another company. Insure your business against theft with a crime and fidelity insurance policy.

The more you know about employee theft, the better you will be able to protect your company. Download the complete 2018 Hiscox Embezzlement Study™: An Insider’s View of Employee Theft.

Related Articles

Event planner insurance: The security you need to balance risks

As an event planner, it’s imperative to bring the same eye for detail to protecting your business as you do for your clients’ events. See what types of insurance policies are best for event planners.

Read More

What is Primary Insurance?

Learn the difference between primary and excess insurance, how primary coverage works, and why clients require primary policies.

Learn more

Learn the difference between primary and excess insurance, how primary coverage works, and why clients require primary policies.

Why do you need fitness trainer insurance?

Learn about the insurance every personal trainer needs to have. Protect your personal training business with personal trainer insurance.

Read MoreWe provide tailored insurance for the specific risks you face, so you can take the right risks to grow your business.

Subscribe to the Hiscox Entrepreneurial Digest on LinkedIn

Get valuable business resources, timely tips and inspiring success stories in your LinkedIn feed every month.